When you think about people getting scammed, you probably think of the elderly getting conned out of money over the phone.

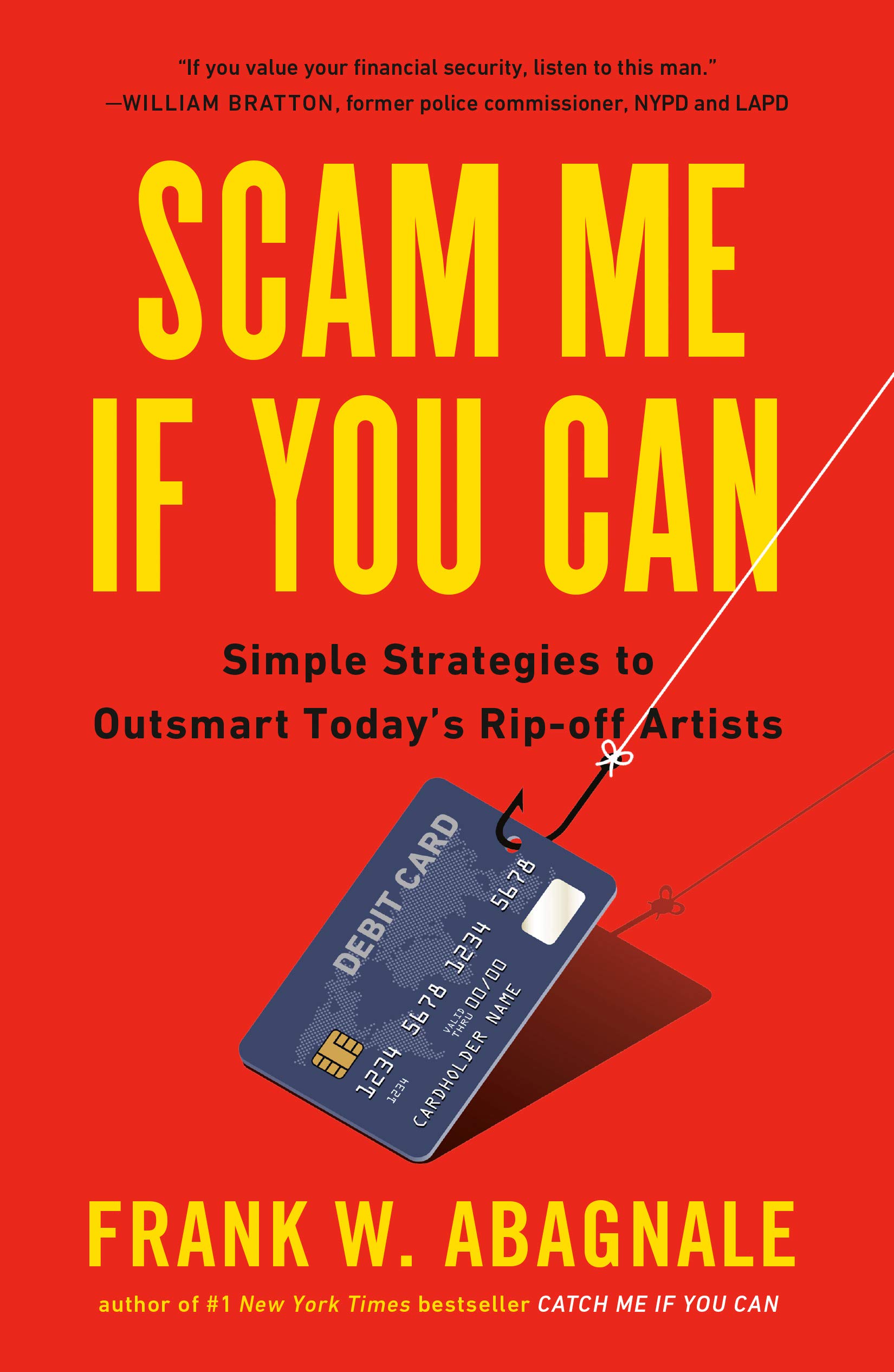

But my guest today says that Millennials are actually more likely to get scammed than senior citizens, and in fact, anybody of any age can get conned. He should know: he’s a former con man himself. His name is Frank Abagnale and his early life in which he forged checks and assumed various identities, including that of an airline pilot and doctor, was made famous by the movie Catch Me If You Can. After he served time for his crimes, he dedicated the next 50 years of his life to helping the government and businesses fight fraud. His most recent book, Scam Me If You Can: Simple Strategies to Outsmart Today’s Rip-off Artists, aims to educate regular citizens about the most common scams out there and how to avoid them. Today on the show Frank gives us the inside dirt on a bunch of different modern cons, from romance scams to investment fraud to scams involving rental properties. He reveals the insidious ways that scammers have gotten more sophisticated with their cons, the red flags to look for when you’re approached with one, and how to avoid getting duped. And he explains why he’s never used a debit card.

Show Highlights

- How Frank ended up as a young con artist

- How Frank then turned that into a career as a security consultant

- The changing nature of Frank’s work as technology has developed

- Why millennials are scammed more often than seniors nowadays

- High-level strategies that all scam artists use to gain your trust

- Two red flags that always pop up with scam artists

- How kids’ identities are getting stolen nowadays (and what parents can do)

- How to spot investment frauds

- Why you should never trust a phone call from a “government agency”

- Balancing convenience and security

- Why Frank doesn’t use a debit card

- How do vacation rental frauds work?

- Why are inheritance scams on the rise?

- Why it’s important to tell someone if you’re being scammed (even though it’s embarrassing)

- What does cryptocurrency fraud look like?

Resources/People/Articles Mentioned in Podcast

- The Psychology of Scam Artists and How to Not Get Duped

- So You (or Your Wife) Wants to Join a Multi-Level Marketing Company

- My Friend Anna by Rachel DeLoache Williams

- Going Undercover: How to Protect Your Privacy Online

- Understanding Credit

- Managing Your Online Reputation

- Bernie Madoff

- Getting a vacation rental? Watch for scams.

- How to Identify Cryptocurrency and ICO Scams

Connect With Frank

Listen to the Podcast! (And don’t forget to leave us a review!)

![]()

Listen to the episode on a separate page.

Subscribe to the podcast in the media player of your choice.

Recorded on ClearCast.io

Listen ad-free on Stitcher Premium; get a free month when you use code “manliness” at checkout.

Podcast Sponsors

Art of Manliness Store. From t-shirts, to mugs, to posters, and other unique items, the Art of Manliness store has something for everyone. Use code “aompodcast” for 10% off your first purchase.

Everlane. Never overpay for quality essentials. My favorite is the Pique Polo. Go to everlane.com/manliness to check out the collection and get free shipping on your first order.

Thursday Boots. A bootstrapped startup that handcrafts boots and sells them direct to consumer. The highest quality at honest prices. Visit ThursdayBoots.com, use code “manliness” to get free 2-day shipping, and while you’re there, check out my favorite, the Vanguard.

Click here to see a full list of our podcast sponsors.

Read the Transcript

Brett McKay: Brett McKay here, and welcome to another edition of The Art of Manliness Podcast. When you think about people getting scammed, you probably think of the elderly getting conned out of money over the phone, but my guest today says that millennials are actually more likely to get scammed than senior citizens. And in fact, anybody of any age can get conned. He should know, he’s a former con man himself. His name is Frank Abagnale. In his early life, which he forged checks and assumed various identities including that of an airline pilot and doctor was made famous by the movie Catch Me If You Can. After he served time for his crimes, he dedicated the next 40 years of his life to helping the government and business fight fraud.

His most recent book, Scam Me If You Can: Simple Strategies to Outsmart Today’s Rip-off Artists, aims to educate regular citizens about the most common scams out there and how to avoid them. Today on the show, Frank gives us the inside dirt on a bunch of different modern cons, from romance scams to investment fraud to scams involving rental properties. He reveals insidious ways that scammers have gotten more sophisticated with their cons, the red flags to look for when you’re approached with one, and how to avoid getting duped. And he explains why he’s never used a debit card. After the show is over, check out our show notes at aom.is/scam. Frank joins me now via Skype.

Frank Abagnale, welcome to the show.

Frank Abagnale: Great. Glad to be here. Thank you.

Brett McKay: So you just come out with a book called Scam Me If You Can: Simple Strategies to Outsmart Today’s Rip-off Artists, you began your young life as a con artist who’s made famous by the movie, Catch Me If You Can. For those who aren’t familiar with your story, how did you get started running these big frauds when you were just a teenager?

Frank Abagnale: I ran away from a broken home. I ended up in court and the judge asked me to choose between which parent I wanted to live with, I didn’t think that was a choice that a 16 year old boy could make, so I ran away. Unfortunately, a lot of kids ran away in the 1960s, but got into Haight-Ashbury, the hippie scene, the drug scene. I ended up on the streets of New York City, 16 years old, and I quickly realized I had to get creative if I was going to survive. I knew that nobody wanted to deal with a 16 year old, and the only advantage I had is I looked a little older, I had a little gray hair. People always told me I look much older. So I basically altered my date of birth on my driver’s license.

Back then they didn’t have a photo on it, it was an IBM card. I was actually born in April of 1948, but I was able to drop the four and convert it to a three, and that made me 10 years older and started acting like a 26 year old. I did have a checking account, because I had done some work in my dad’s store and he put money in an account for me. So I started writing checks, and I found it very easy to go in and talk people into cashing a check for me. When there was money in the account, they were good, but when the money ran out, I found this just as easy going in and writing those checks even there wasn’t any money behind it. And that started me off knowing that people were chasing me as a runaway, they were chasing me for writing bad checks.

And then I realized that I had to stay one step ahead of those people and that started my career off of crime and doing all the things I did between 16 and 21.

Brett McKay: Right, that was imitating you were a pilot, doctor, all those things. How did you turn into a consultant? Because now what you do is you help companies and the government avoid getting scammed, how did that happen?

Frank Abagnale: Well, what happened was that I was arrested at 21 by the French police. I was convicted of forgery in France and sent to French prison. When my sentence was over, I was immediately extradited from the French prison to Sweden where I was convicted of forgery and sent to a Swedish penitentiary in Malmo, Sweden. And when my term was up there, US federal authorities took custody of me, returned me to the United States, and the US federal judge sentenced me to 12 years in federal prison. I served about four of those 12 years at a federal prison in Petersburg, Virginia, and when I was 26 years old, the government offered to take me out of prison under the condition that I go to work with an agency of the federal government.

I agreed, and it was for the time of my sentence or until my parole had expired, I have been at the FBI now for 43 years, for more than four decades. I started out teaching at the FBI Academy and working with the FBI, and I soon realized that I had a lot of knowledge that was not just good for training FBI agents, but it was good for going out and teaching banks and corporations how to protect their money and their assets. And so all my career, I’ve had the opportunity to work with more than 50% of the Fortune 500 companies, and I’ve had the ability to go out and develop technology that went into paper and plastic, and today, do a lot with software technology.

I’ve had to change as crime has changed a lot from 40 years ago, and I’ve had to change with crime and figure out how crime works now versus then. This book, Scam Me If You Can is one of five books I’ve written, the other books have all dealt with commercial crime, forgery, embezzlement, things of that nature, this is the first time I wrote a book concerning consumers and scams committed against all types of consumers. So it’s been a little bit different but been great.

Brett McKay: Also you mentioned you’ve had to change how you approach things, your business and what you’re looking at, I mean, you primarily took part when you were doing fraud, it was in the 1960s, what’s changed since then? And what’s changed in maybe the past 10 years?

Frank Abagnale: Nothing’s really different in the scams themselves. They’re all basically the same, the same way we con people and scam people. The only difference is technology has made it so much easier. Back when I did social engineering and of course, I didn’t realize I was social engineering anybody, but back then I only had a phone. Today, there are many forms of communications, and of course, the ability to scam someone from thousands of miles away, so you don’t have the concern of being caught, apprehended and prosecuted. Of course, you never see your victim, your victim never sees you, so there’s no emotion involved, there’s no compassion involved for the victim.

So unfortunately, it’s very scary because people will steal your money and steal everything you have, versus 50 years ago when you had to deal with someone one on one and maybe had a relationship with that person. So there was a little bit of compassion, a little bit of emotion, that’s gone out the door.

Brett McKay: And what’s the state of consumer fraud in America? Has it been on the uptick dramatically or has been a slow increase? What does that look like?

Frank Abagnale: It’s absolutely on the uptake, and billions and billions of dollars committed in scams every day, not just against seniors. In doing the research for this book, one of the things that amazed me was that millennials are actually scammed more often than seniors, but seniors lose more money. And so as I remind people all the time, anybody can be scammed. I know I can be scammed, anybody can be scammed. The main thing is to basically try to educate yourself so that you understand how some of these things work. And anytime you’re going to part with your money or part with personal information about yourself, you need to know who you’re giving that information to before you depart with any of that money.

Brett McKay: That was an interesting point, because typically when you think of victims of fraud you think of elderly people, they get the phone call saying they owe an IRS bill. But I thought was interesting that millennials are actually scammed more than elderly people.

Frank Abagnale: Yeah, especially on computer scams where they’re sitting at their screen and a pop up comes up says, “This is Microsoft, we believe you have malware on your computer, call this 1-800 number.” And they call and say, “You need to pay 39.95, give us your credit card over the phone.” I think that young people really don’t think these things out, and they don’t really have a deceptive mind, so they think that this is legitimate and it’s okay to do this, it’s okay to give away this information. They don’t really understand how someone would misuse that information or bring them harm through the information they give them.

Brett McKay: So before we dig into specific ways scam artists rip people off and what you can do to protect yourself from them, you begin the book talking about sort of the high level strategy that all scam artists use, no matter their specific tactic or strategy. And the first part of this sort of high level fraud thinking that people use is getting the target under the ether. What do you mean by that?

Frank Abagnale: You get people to truly believe that you are who you say you are. We’ve seen these romance scams more than double over the last few years. You meet someone online, you start to befriend them online, and the next thing you know, you’re talking to them on the telephone, and you start a relationship with them. You might be a little bit lonely, and now you met this very nice person. They’re very kind to you, you have similar things that you like talk about together. And this may go on for a year, 12 months, or more, and eventually, you might say to that person, “So look, Robert, if you only live a couple of states away, why don’t you come over and see me?”

“Well, I would, but I have to have this operation and it’s $30,000, and I don’t have the money. And if I don’t have the operation, I don’t know that I’m really going to make it.” “Well, I could loan you the money.” It’s getting people to start to really believe you are who you say you are, to get you to believe what they’re saying is true. And once you get there, you basically are able to scam those people unfortunately, because they believe that what you’re telling them is the truth. They believe you are who you say you are. And that’s how almost all scams work.

Brett McKay: I mean, there’s specific tactics that scam artists use to build that trust up.

Frank Abagnale: We’ve had the lady here in Manhattan that basically said she was an heiress from Europe, she didn’t have a dime to her name, but she came to New York, she started to realize she needed to meet very important, wealthy people. So she met them, they kind of liked her. She said she was an heiress, that she had all of this money, so then that friend said, “Oh, well, let me invite you to a party I’m having, you’ll meet some really nice people there.” And then she went to that party, she met people, she was attractive, she had a nice personality. People had no reason not to believe her. Those people got to befriend her. They introduced her to other people. She became well known as a socialite New York.

People all believed her to be very wealthy. And these are all about building these scams, building these pyramids, it takes a lot of time, a lot of investment on behalf of the individual. And eventually, she started to tell people that she knew that she was going to invest in certain things, and they said, “Well, I’d maybe like to invest with you with that.” Some people she turned down just on purpose to make them want to do it more. And eventually, she took people for a lot of money. In her case, she never had an end game. She never realized how to get out of it once she got totally in it, so eventually, she got caught. But all these scams and pyramid scams and all that, pretty much work basically the same way.

It’s all about building trust with people. It’s not an overnight thing. It takes a long time. It takes a lot of effort. It takes a lot of time to build relationships with people, but in the end, people are out to get a lot of money from it.

Brett McKay: What that story illustrates well is something you recognized yourself as a con artist, which was that if you look and act the part, people just accept that you are who you say you are. So when you dress and act like a pilot or a doctor, people accepted that. So if you act like you belong somewhere, people figure you do. Another part of this high level strategy that con artists use is using a sense of urgency to get people to do what they want. What does that look like?

Frank Abagnale: Well, here’s the thing. In doing this research for this book, what was important to me was to look at every single type of scam, no matter whether it was Bitcoin scams, cryptocurrency scams, Wall Street scams, scams against seniors, scams against millennials. And in doing so, what amazed me is that I realized that no matter what the scam was, no matter how sophisticated or how amateur it was, at some point, two red flags were going to show up, either one or the other. The first red flag is that I’m going to ask you for money, and I need you to do it immediately, “You give me a credit card over the phone, give me your bank account number so I can draft on your bank.” “Go down to Walmart, get me a Green Dot card, bring the card back and call me right back with the card number on the back.”

Everything had to be immediately, and that’s the first red flag. And the second red flag is that somewhere along the line, like in the romance scam or in any scam, they’re going to ask you for information, “What’s your social security number? What’s your date of birth? Where do you bank?” Personal information. And I tell people, look, you can be involved in a romance online with someone, and that’s great. It goes on for nine months, 18 months, everything’s great, but at some point, when that person starts asking you for money, or they start asking you personal information, you never met that person, you don’t know who that person really is, that’s that red flag. That’s where you need to stop, and make sure before you ever part with any of your money or information, you know who you’re dealing with.

And if you learn these red flags, because in every scam they have to come up, that will alert you that this is probably a scam.

Brett McKay: Right. Those red flags are important, because what I think is interesting about some of these high level tactics that con artists use, building trust, using scarcity and urgency, these are skills that can be used for legitimate purposes, right? I mean, that’s what salespeople do.

Frank Abagnale: Absolutely. I used to tell people, when they say, “You were a great conman or confidence man.” I tell them, “All of the abilities I had are the same abilities that a great salesman has, a great public relations guy has, a great marketing person has.” They’re only using their skills in the right side of the law, and they’re never crossing over that line of legality and what’s legal and what’s not, whereas a con man is looking for a shortcut to an end, and basically is willing to bend the law or break the law to do so. But that’s the only difference in those personalities.

Brett McKay: So let’s talk about specific scams that you talk about in the book, a few of them. One is identity theft, and I think we’ve all read those stories about elderly people getting their identity stolen and racking up these bills that they had to fight for years and years, but what I thought was interesting, for young people who have kids, your child who’s like three years old can have their identity stolen. How does that happen?

Frank Abagnale: Actually, because unfortunately, now every child has a Social Security Number from the day they’re born. Back in my day, growing up, you didn’t receive your Social Security Number till you first got a job, so you were at least 16, 17 years old, and you were issued a Social Security Card Number. No one knew that number except your employer, yourself and the federal government. Now when a baby comes out of the hospital, an infant, they’re assigned a Social Security Number. And for scam artists, they’d much rather have the Social Security Number of a six year old boy than a 60 year old man who might be very wealthy, because the six year old boy has no credit, and for the next probably 10, 12 years, is not going to seek any credit.

So I can actually become the six year old boy for a long time before anybody ever knows I stole their identity. And God forbid I get the social security number of an infant coming out of the hospital, I can use that identity for 18, 20 years, sell it, resell it over and over before anyone ever knows I stole that child’s identity. So children’s identity theft is a big issue. Many people don’t think about that, they think only about wealthy people or older people or established people having their identity stolen, when it’s really, a lot of times, children identities they would prefer to steal. The other thing to remember, stealing identities today has become so simple, because we live in a way too much information world.

I’m not on social media of any kind, but if you’re on Facebook, and you tell somebody when you were born and your date of birth, that’s 98% of stealing your identity, so you make it so easy for people. I always tell people, you never want to state where you were born and your date of birth, otherwise, you might as well say, “Come steal my identity.”

Brett McKay: So what can parents do to help their kids avoid identity theft?

Frank Abagnale: They need to teach their children about giving information away, saying too much. If they’re going to be on social media, they shouldn’t be telling people personal information about them. Certainly not saying where they were born or their date of birth, being careful what kind of picture they post on their social media. If you’re using a passport style photo, a graduation photo or even a driver’s license style photo, through facial recognition tools, they can take a picture of you that brings them to your Facebook page, they can take that picture from your Facebook page and use it on some other form of identification.

A lot of romance scams, what we find is there’s a picture of a young Marine on Facebook, and he’s highly decorated, great looking guy, he’s in full uniform, he looks magnificent, it’s a straight on portrait of that person. They will then take that photograph, send out thousands of emails to women saying, “This is me. Here’s a picture of me, and I’d like to get to meet you.” And they really think that they’re involved with that person in the photograph, when really it’s probably maybe an 80 year old guy on the other end who’s doing that. And eventually, of course, they say, “I’m over at Afghanistan, I don’t have access to money, could you get me a debit card, or go to Walmart, buy a Green Dot Card and read me the number so I could have some access to money to buy some things over here.”

There are so many scams built around things like that, so you have to be very careful. And of course, I always tell young people, you have to be careful what you say and what you post on things like Facebook. So if you have a picture of you nude on the beach with a bunch of drug paraphernalia all over your body and wine bottles and whiskey bottles, one day when you go applying for a job, we know that 70% of Fortune 500 companies look at your Facebook page, and do you want them to see that picture? If you say something about someone sexual orientation or someone’s race when you’re 12 years old, because you don’t know any better, do you want your employer or your school of admissions to read that or see that later?

Because the fact is you can erase it, you can delete it, you can close your account, but it’s retrievable. So I always tell young people, before you post, before you make a statement, you might regret, you need to ask yourself, do you want someone to read this five years from now, 10 years from now? You got to be a little smarter and a little wiser today than you did 20, 30 years ago.

Brett McKay: So another common consumer facing fraud that you’re seeing an increase of is investment frauds? What are the typical type of investment fraud you see in your work?

Frank Abagnale: It’s people that you encounter that talk you into investing money when you really don’t know a lot about that individual’s background. Anybody could defraud you, but usually, if you’re going to make an investment with someone, you want to make sure that you’ve checked out their references, the people that they have dealt with for many years and what they have to say about them, what that person’s track record is in making those investments. Are they tied to a legitimate company, a big brokerage house or a financial institution or someone that’s an established company that you know the person has had background checks, people know who they are?

I’d be very leery of just meeting someone or someone I didn’t know a lot about, and maybe they impressed me because I think they have a lot of money, and they make me believe they’re very good at what they do, and putting money with them. Because, again, you have to take a little time before you part with your money or information and make sure you know who you’re giving it to. Today, with all the resources we have out there with the internet and things of that nature, it’s not difficult to make some calls and check things out before you ever actually go give anybody any of your money.

Brett McKay: Well, and the tricky thing is that sometimes fraudsters who are trying to run investment fraud, they understand that people aren’t going to trust me right away, so they’ll use the friends of these people they’re trying to target to build up that trust. That’s what Bernie Madoff did with his affinity fraud.

Frank Abagnale: And what most scam artists do. So they start out to build a relationship with people who have influence. And every one of these scams that we see basically, even the big, big scams like the people who said they invented the blood test that you just have to prick your finger and you don’t have to have your blood taken anymore, got involved with people in the military, generals. They got very prestigious people involved, so that they were really selling the scam unknowingly for them. They’re building that credibility through people they know or people they have a relationship with. But again, you have to be a little bit more careful.

I just can’t make an investment because someone told me that this guy’s good, or this guy I’ve made investments with, I’ve always got a return on my money. I still want to go a little deeper than that. I want to know how long this person has been around, what’s their reputation. You got to take the time to do a little bit of research and take a little time to investigate before you depart with your money.

Brett McKay: I think people have heard that advice, like if someone’s promising you like 125% returns, that’s probably a scam. But there’s some investment frauds that a little more sophisticated and they’re harder to detect. And one you talked about is churning. What is that?

Frank Abagnale: This is basically where people get other people, so for example, I might say to you, “Hey, you want to invest $50,000 with me, I think I’ll be able to double your money in about six months.” And for whatever reason you trust me, you give me the 50,000, and certainly six months later, I turn to you and say, “Hey, here’s your 50,000 plus the 50,000 more that I told you you’d get.” Well then you’re going to tell some other friend, “Yeah, I invested with Frank and gave him $50,000, and then six months later, I made $50,000. It was great.” I’m using the influence of those people, you are my tool, basically to convince other people that I’m legitimate, and I might do that with several people.

And that’s kind of what Madoff did as well. He did turn people’s money around. He made 33% on a lot of people’s money. These were very influential people, and when someone said to another guy, “Well, look, if you need your money from Bernie, how hard is it to get it?” “No, I call him at 10:00 in the morning, I tell him I need a million dollars I’m closing on a house in the afternoon, and by 2:00 the money’s in my bank account, no questions asked.” Those are the people that he uses to sell the people that he’s really going to end up taking.

Brett McKay: And another one that’s very subtle is, say, you invest with a fund manager, what they do is they make a lot of transactions that they don’t need to make, because every transaction they make, they’re making money off of you.

Frank Abagnale: They collect fees.

Brett McKay: Right.

Frank Abagnale: Yes, and they’re just doing it to collect those fees. Technology has helped so much. I talk in the book about the grandparent scam. There are so many people who fall for the grandparent scam. And what happens is the phone rings in the evening, you look on the phone, and it says it’s the police department, of course you can manipulate caller ID to say anything you want it to say, US Treasury, IRS, Medicare. So first, you believe immediately that it is the police department, so you pick up the phone, they say, “We arrested your grandson, he was DWI. We have taken him into custody. He was in this type of vehicle.” And you say to yourself, “Oh yeah, that’s his car.”

“He had a passenger in the car. It’s this young lady.” And you go, “Oh yeah, that’s his girlfriend.” “We were going to call his parents,” and they tell you the parents name, and you go, “Yeah, that’s right.” “But he asked us not to call his parents, he asked us to call you, and he needs to post bail in the next two hours, or he’ll have to spend the weekend in jail.” “Well, I don’t want that to happen, what do I have to do to post bail?” “Well, you can give me your credit card over the phone, and we can post a $500 bail.” “Okay, I’ll be happy to do that.” These scam artists have come a lot more sophisticated over the last few years, they go to social media, the grandson already has pictures of his car up on Facebook.

He has pictures of him and his girlfriend and her name. He has pictures of his family and their name. That builds so much credibility into whether it’s a phishing email or whether it’s just that phone call, that you really, truly believe this must be the police. But again, at this point is that red flag, where even if you said to the police department, “You know what, I live just a block from the police department, so let me just come down there right now and I’ll bring you the money.” “Oh, no sir, you can’t do that. You have to pay over the phone, you have to use your credit card, has to be now.” That’s the time that you need to hang up, look up the police department’s phone number, call the police department, tell them about the call you received to which they’re going to tell you that that’s a scam and to ignore it.

But that’s where you have to be smart enough to do that before you give out that information or give out that money.

Brett McKay: Well, yeah. You talk about different scams that people use the government to get the money, and oftentimes what they use, like a red flag is if you have a government agency asking you for information or money over the phone, it’s probably a scam.

Frank Abagnale: A red flag. First of all, government agencies are not going to call you. I explain to people all the time, for example, Medicare, when you turn 65 and you sign up, you have to fill up all these forms, and of course, you’ve put in your address and your phone numbers and all that, as soon as they put that into their system, the first thing that Medicare deletes is your phone numbers. They don’t have your phone number, because they have no reason to call you, and they’re not going to call you. So the minute someone calls and says they’re from the IRS or they’re from Medicare, you know that’s a scam. Now, be careful because all scam artists work a scam for a while, and then when they realize the scam has got a lot of attention, a lot of people know it’s a scam, they switch gears a little bit.

So now they’re apt to send you a letter, which looks very official, comes on what supposedly is an IRS letterhead, the envelope on the outside says, postage and fees paid by United States government, return address is the US Treasury, and you open it up and it says “We need to speak to you immediately. If we don’t hear from you in this many days, we’ll have to file a lien on your bank account. Please call the 800 number below and ask for agent so and so.” 800 number is a boiler room in Miami, they answer, a young lady, very nicely, “Internal Revenue Service, how can I help you?” “I received this letter.” “There should be a reference number up in the corner.” “Yes, I have it.” “What’s the number?” “Yes, sir. That’s agent Johnson, let me turn you over to him.”

And they collect calls to another table where the other scam artist picks it up, goes, “Agent Johnson.” And it’s the same scam, only they’re making a little more believable. Yesterday, on the front page of The Wall Street Journal, there was a new scam going around where they’re calling people with student loans, and saying, “We can negotiate your student loan down, we can negotiate your payment down, your interest down, but it’s $1250 for our services.” Well, first of all, those are just scams. If you would actually give them the money, you’ll probably never hear from them again. And even if they were in fact a semi legitimate company, everything they’re saying that they can do, you could do yourself, you don’t need them to do it. You could call and renegotiate. You could get your interest rate down.

You could do those things on your own. So that’s just another scam. Every time there’s something going on, like student loans or new Medicare cards or anything like that, then the scam artist are out there partaking some scam around that new thing that’s out there.

Brett McKay: So what’s the red flag if you get that fake letter from the IRS? How do you know it’s a fake?

Frank Abagnale: Again, you don’t really know it’s a fake, so again, you need to call, but you need to go look up the number of the IRS and actually call the IRS office and explain to them that I received this letter. They are going to ask you what the reference number is up in the right hand corner, because that’s how the IRS and many government agencies work, and they’re going to say to you, “Sir, that’s a fictitious number that doesn’t belong to us, and there is no agent Johnson at that phone number that you read to me that they gave you on the letterhead. That is just a scam, and don’t answer or respond to any information that they’ve requested from you.”

You have to just take that whole thing of stop and verify. Again, if everything’s fine until I start asking you for money, or I start asking you for information, that’s when you really need to stop and verify that that is who they say they are and that it’s real.

Brett McKay: Yeah. I think that’s for everything, even just personal security, you have to put up barriers. You have to make things a little bit more inconvenient for yourself, if you want to maintain security.

Frank Abagnale: Right. And there is no such thing as convenience and security, you can’t have both. So you either have security or you have convenience. So if it’s your personal security, that should be number one. You should be thinking about how safe you can make it for yourself, and doing that so that you protect yourself as number one. I do a lot of simple things, for example, I’ve written a lot about the fact that I only use a credit card, I don’t own a debit card, never owned a debit card. And the credit card I use is in fact a credit card, not a credit debit card. I do that because I know that no matter where I go in the world, if someone gets my number and charges a million dollars on my card tomorrow, by federal law, I have no liability.

If I buy something online and they don’t deliver it, credit card company makes it good. If I purchase something online and it comes broken, but the company refuses to take it back, the credit card company makes it good. When I pay the bill or the minimum due, I raise my credit score, my score keeps going up. When you use your debit card, every time you reach for it, you’re exposing the money in your account. And so in every breach that we’ve had, way back to TJ Maxx 15 years ago, when they’ve gotten the credit card number, when you interview in a post investigation, the person says, “Well, no, I used my visa card, and actually they canceled it the next day, and then two days later I got a new car, and that was the last I heard about it.”

“Oh no, I used my debit card off my credit union, they took $3,000 out of my checking account, and it took me about three months while they were investigating to get my money back.” So to be honest with you, even when I go to an ATM, especially overseas, I withdraw money on my credit card. Yes, they charge me a fee, but I look at that as cheap insurance that no one is getting into my account. My account is not being exposed to anyone, and they’re not going to get my money. So common sense things like that, that you look at what eliminates the risk. So if I’m going to use Venmo or any of those kind of payment forms, I’m going to back those by a credit card, not backed by a debit card, because I don’t want someone to have access to my account.

Now, I truly understand that there are people who can’t handle their money very well, they’re not good at paying their bills, well, then those people should stick with a debit card. But if you’re good at handling your money, and you’re good at paying your bill and what’s due when it’s due, then it’s much better off using a credit card.

Brett McKay: A scam you talk about that I didn’t know existed, but I’ve used these services a lot is vacation rental websites like Vrbo or Airbnb. Some of these websites have frauds running on. How do the frauds work on these vacation rental sites?

Frank Abagnale: Oh, constantly. As a matter of fact, I just had dinner a few nights ago, I live in Charleston, South Carolina, a young man who grew up in Tulsa, I was a godfather to his sister, know his family very well, known him since he was a baby, he’s working on his master’s program, so he is coming to Charleston for one year to finish his master, and he was telling me, he said, “You cannot believe all the scams when I was trying to rent an apartment. All these people wanted me to send them a $1200 deposit. It was just by email, you didn’t see them, you couldn’t talk to them on the phone.” And he said, “My friend, went and made the foolish mistake of sending $2500 to one of those people, and then when he got to Charleston, the place was not for rent, it never had been for rent, and he’s out his $2500. He doesn’t even know who that person was, because he only dealt with them on email.”

And yes, these things happen all the time. I send you pictures of the place, I send you all the information about the place, it looks very legitimate, and then the red flag is that I’m telling you that there is a deposit, and you need to make the deposit up front. And again, if I was in that situation, I’d have to say to the person, “I’m going to have to wait till I get down there, see the place and then I will be more than happy to sign the lease and give you the money. I don’t feel comfortable sending the money. I’ve not been there. I don’t know that this is a real place. I don’t know who you are.” And that’s what he did. He waited till he got here, a young lady had the place, he looked at it, you knew it was her place, and then he gave her the deposit and took the apartment.

Brett McKay: I mean, would another strategy be, only interact on the website itself and don’t take it off the website? It’s sounds like if you just go to email and work directly, you increase your chances of being defrauded.

Frank Abagnale: Absolutely, because you don’t know who’s on the other end of that email, and of course, we know there are a lot of phony websites, and I can create really very impressive replicas of real websites. But again, you want to make sure that you’re doing business with somebody that’s real, so you want to go check it out. I mean, those are simple things. If I was doing something like that, I might call a real estate office down there and ask if this property exists, or you can call the Better Business Bureau and say, “Did you have complaints of people selling these apartments or this address and not absconding with the money?” There are many ways to check those things out, but I again, would say that that’s what I would do before I parted with any kind of money.

Brett McKay: So one scam we’re probably seeing more of right now, because baby boomers are retiring, and there’s going to be this huge transfer of wealth coming up pretty soon is the inheritance scams.

Frank Abagnale: Yeah, inheritance scams and scams of all kinds. I know people don’t like to hear this because they think it sounds simplistic, but having done this now for 43 years on this side of the law, written books about it, articles about it, having been involved in cases all over the world, having worked with AARP for the past five years on these problems with these crimes, the one thing that really comes back to me all the time is that we live in an extremely unethical society. We live in a society where we don’t teach ethics at home. We live in a society where we don’t teach ethics in school, because the teacher would be accused of teaching morality.

We live in a society where you don’t get in a four year college or course about ethics, only one son who went to law school got a course on ethics. And in most companies, there’s a code of ethics, a code of conduct, but it’s just printed on the back of the annual report. It’s not really instilled in their employees. So we’ve come along now to generations of people who have really no ethics, no character, and it’s all about me. It’s all about greed, “What can I do to enhance me? And if I have to step on somebody or I have to hurt somebody, or especially somebody I never even met, I just know online, I’m willing to do that.” And until we change that attitude …

And this has nothing to do with religion, it’s just the difference between what’s right and what’s wrong. Until we start bringing that back into our homes, back into our schools, back into our universities, crime is just going to get easier, because technology will always make crime easier, will always allow the criminal to do things. As well as technology stops crime, it’s also very easy to commit crimes with technology. So you have to stop the way people are thinking and the way people perceive things, and the way people interact with other human beings, otherwise, it will just continue on this cycle forever.

Brett McKay: Right. And I guess with the inheritance scams, if you have older parents, make sure they have a will in place, a trust in place, all those-

Frank Abagnale: They have a will in place. I don’t know how many cases I have where somebody has an aid or a secretary, they’re 82 years old, and the next thing you know, they pass away and all the money’s been left to the aid or left to their secretary or assistant, and the will’s been changed maybe a year earlier or six months earlier. And they say, “Well, no, he wanted to give me everything.” That’s hard to believe that he didn’t want to leave his children anything. But people do that, and sometimes people get away with that. So you always want to be making sure your family, especially older members of the family are protected.

And what happens, unfortunately, with a lot of these scams is that maybe Mrs. Johnson, who’s 78 years old falls for a sweepstakes scam and loses $5,000. Well, she’s afraid to tell her loved ones because then the daughter says, “See mom, you can’t really handle your money. I need to take over your checkbook, all your finances and basically take away your independence.” They’re afraid to tell the police because it might get out in the news and then her friends will know that she was scammed out of this money. So when we look at the billions of dollars in scams, crimes against the elderly, we only know what we know to be facts. We don’t know all of the people who didn’t report it, and most people don’t report it.

I always remind those people that there’s nothing to be ashamed of, anybody can be scammed, the most intelligent people in the world get scammed. I know I can be scammed. But if you’re scammed, you need to tell somebody so that something can be done about it. If you don’t tell anybody, they’re just going to go on and scam somebody else.

Brett McKay: I know some states are actually passing laws to help prevent scam on elderly people, so like if there’s a sudden transfer of wealth in a certain amount of time, they’ll actually retro actively say, “No, that doesn’t count,” or something like that. I think Florida is doing that.

Frank Abagnale: Right. And what’s happened, and how I really got involved with all of this, AARP has 38 million members, so a number of years ago in a survey out to their members, they asked them what was some of their concerns, and they were amazed that they came back saying that they were concerned about identity theft, falling victim to these scams, losing their life savings. And so they went out to find out what information was available out there in the marketplace, and there wasn’t really a whole lot about it. So they came to me and I started working with them five years ago. They developed what’s called the Fraud Watch Network, and developed educational materials, training materials.

They asked me and commissioned me to write this book for them, all the proceeds from the book and the advance for the book and the royalties of the book will go to AARP. And basically, they have gone out and set up the Fraud Watch Network. They have a call center in Denver, Colorado, where you can call the 800 number and speak to a volunteer there, that’s very knowledgeable, if you think you’ve been scammed or you’re thinking of investing in a charity but you’re not sure if the charity is legitimate, or you got this phone call and you’re not sure that the phone call is real and it might be a scam. But you don’t have to be an AARP member, you could be 18 years old and call.

I’ve been to 40 states on their behalf speaking to groups, thousands at a time, sometimes in major cities, and anyone can come. There’s no fee to come. They’re not selling you anything. They don’t allow you to sell anything. It’s strictly to help educate people. And so this has been very rewarding for me to be able to do something a little different in my career, and not just protecting businesses and corporations and banks and governments, but being able to go out and help the people who really need the help, people who can be victimized. Whether they be a millennial or whether they be a senior, to help educate them so they don’t fall victims to these crimes.

So there’s a lot being done both on the law enforcement side, as well as being done on groups like AARP who have taken upon themselves to help fight some of these crimes.

Brett McKay: So let’s talk about one last crime that hadn’t existed maybe five years ago, but now you’re seeing more of, and that’s cryptocurrency fraud or Bitcoin fraud. What does that look like?

Frank Abagnale: Yeah, because it’s not very safe. Last year, we shut down more than 100 exchanges that turned out to be fraudulent exchanges. A lot of these Bitcoin sites can easily be hacked into. There’s no real good internal security, so people lose all of their money in a matter of seconds by someone that’s hacked into it or someone pulled a scam doing that. I was asked many years ago in Atlantic magazine where on the last page of their monthly magazine, they ask a noted person a question and one response, and they asked me what I thought about Bitcoin, and I said I felt it was actually one of the biggest scams perpetrated against the people of the world.

It’s just basically not safe. It may be safe someday, but it’s now just a way to hide money, to launder money, to use illegal money and get it to turn into proper money. There’s a lot of issues with Bitcoin. So I think it’s very risky, but again, it has a high return. People get greedy, they’re willing to take the risks, and it can be very harmful if you obviously lose all your money.

Brett McKay: Well, Frank, we’ve just scratched the surface with this. Where can people go to learn more about the book and your work?

Frank Abagnale: Scam Me If You Can is in the bookstores on Amazon, and basically my website is just abagnale.com, very simple, my last name .com. I write about a lot of things, I put them up on my website. I try to make sure they’re timely. Every interview I do in print, I publish it up on my website so people can go see what I had to say about it. There’s information on my website about how to spot a counterfeit bill, how to spot a short change artists, how to use credit properly, identity theft, all of these issues. And in Scam Me If You Can, I truly took the time and effort to recognize every type of scam, explain it in very simple language.

I wanted the book to be a reference book too for police officers, social workers, even individuals who can go five years from now and say, “I think this is a scam. I think I read something about that, I’m going to look this up and see if this is actually a scam.” And that was the purpose of the book. And so I’m a big believer that education is the most powerful tool to fighting crime. And if you educate yourself, you make yourself more aware of your surroundings and what’s going on around you, you’re going to be better off doing that. So I hope this book is just one way of helping people achieve that.

Brett McKay: Well, Frank, thanks for your time. It’s been a pleasure.

Frank Abagnale: Thank you. It’s great talking to you again.

Brett McKay: My guest today was Frank Abagnale. He’s the author of the book, Scam Me If You Can. It’s available on amazon.com and bookstores everywhere. You can find out more information about his work at his website abagnale.com, that’s A-B-A-G-N-A-L-E.com. Also check out our show notes at aom.is/scam, where you can find links to resources, we can delve deeper into this topic. Well that wraps up another edition of the AOM Podcast. Check out our website at artofmanliness.com where you can find our podcast archives, there’s almost 500 episodes there, as well as thousands of articles we’ve written over the years, from personal finance, physical fitness, how to be a better husband, better father.

And if you’d like to enjoy ad free episodes of The Art of Manliness Podcast, you can do so on Stitcher Premium. Head over to stitcherpremium.com, sign up, after you’ve signed up, you can download the app on Android or iOS. And when you sign up, use code manliness to get a free month trial Stitcher Premium, so don’t forget that. stitcherpremium.com, and you can start enjoying ad free episodes of The Art of Manliness Podcast. And if you haven’t done so already, I’d appreciate if you take one minute to give us a review on iTunes or Stitcher, it helps out a lot, and if you’ve done that already, thank you. Please consider sharing the show with a friend or family member who you think would get something out of it.

As always, thank you for the continued support and until next time, this is Brett McKay reminding you not only to listen to the AOM Podcast, but put what you’ve heard into action.